This proposal is part of the 2.03 upgrade process, please comment by replying below.

Standard

Activity

**Schema Object** Codelist

**Type of Change** Change code descriptions

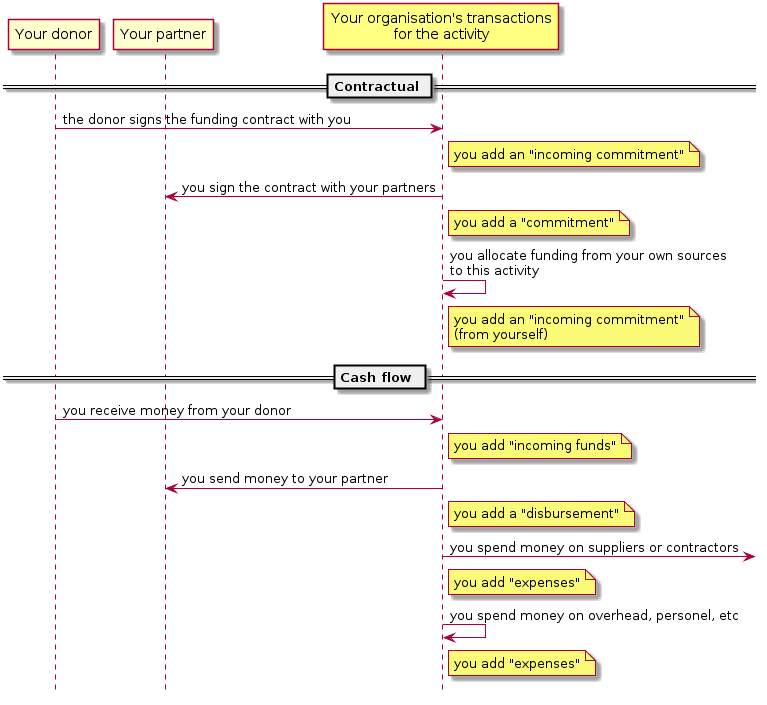

**Issue** Clarify the distinction between disbursements and expenditures

**Proposal** Make the following changes to the [TransactionType](http://iatistandard.org/202/codelists/TransactionType/) codelist descriptions:

- Disbursement

- From: “Outgoing funds that are placed at the disposal of a recipient government or organisation, or funds transferred between two separately reported activities.Under IATI traceability standards the recipient of a disbursement should also be required to report their activities to IATI.”

- To: “Outgoing funds that are transferred to a recipient organisation that reports, or is expected to report, their activities to IATI; or funds transferred within an organisation between two separately reported activities.”

- Expenditure

- From: “Outgoing funds that are spent on goods and services for the activity. The recipients of expenditures fall outside of IATI traceability standards.”

- To: “Outgoing funds that are spent on goods and services for the activity, or are transferred to a recipient that doesn’t and is is not expected to report their activities to IATI.”

**Links** N/A